Bed Bath & Beyond Products Are Already Cheaper Than Amazon! - Bed Bath & Beyond Inc. (NASDAQ:BBBY)

Most Americans have heard of Bed Bath & Beyond (NASDAQ:BBBY) that sells a wide collection of domestic merchandise and home furnishings through over 1,000 of its namesake stores. What people may not know is that BBBY products are cheaper than Amazon (NASDAQ:AMZN) before applying any coupons. With 20% coupons or its new membership program, it's not even close!

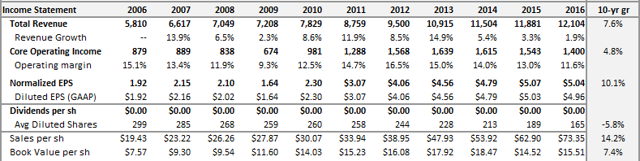

Before we go into the research I did on product prices, let's look at some company fundamentals, comparables and valuation. Over the last 10 years, BBBY has grown revenues, operating profits and EPS by 8%, 5% and 10% respectively.

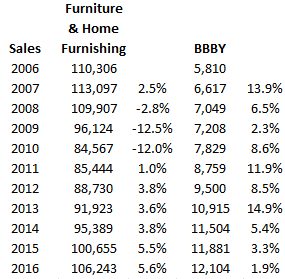

If we look at U.S. Retail Sales and specifically "Furniture and Home Furnishing stores," we see that BBBY has exhibited better growth than the category for every year except the last two.

The company has grown year after year, despite the competition, which has had its effect on margins (11.6% in FY16 vs. 16.5% in FY12). Street expectations are for another year of small growth but margins are expected to get even tighter. This trickles down to cash flow and while the company generated $0.8-1.1bn in free cash flow in FY12-15, this came in at $684m in FY16 with expectations of $600-700m for the next 2 years.

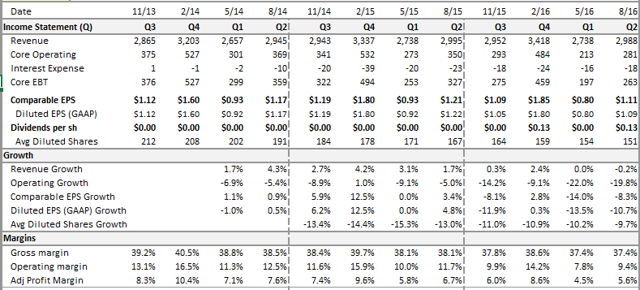

Over the last four quarters, sales have been stable but operating profits have suffered with LTM operating margin 200 bps lower!

As a result, the stock price has declined and is at a new yearly low. The last time BBBY was at such prices it was 2010! Since 2010, operating profit and EPS are 43% and 119% higher respectively.

(Source: StockCharts.com)

(Source: StockCharts.com)

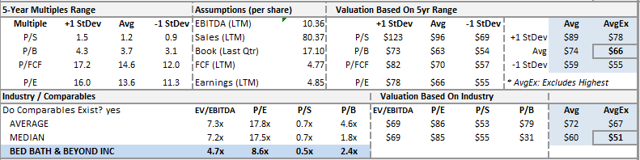

Looking at the 5-year market multiples range the stock has traded at, we see it is below the low end (which would value it at $55). If the stock price were to return to its average or industry valuation, it would be trading at $60-70.

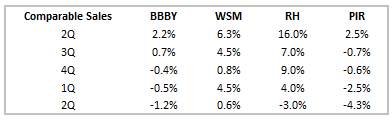

Compared to Williams-Sonoma (NYSE:WSM) and Restoration Hardware (NYSE:RH), BBBY comparable sales have been worse and have only beat Pier 1 (NYSE:PIR). It should be noted that all three of these companies are much smaller with last twelve-month sales of $5.1bn, $2.2bn and $1.8bn respectively.

Still, if we assume $650m in free cash flow in a zero growth perpetuity, the stock would be worth $54. We can only conclude that the market has priced in a pretty dim future for the company.

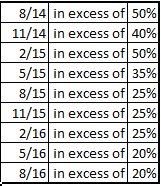

Investors have raised concerns over online competition, but if we look at the company filings, we will find that online sales at BBBY are doing extremely well. In the last 9 quarterly filings, we find that online sales have been growing at 20-50% year on year. For example from the last 10-Q "...comparable sales consummated through customer facing online websites and mobile applications increased in excess of 20% over the corresponding periods in the prior year..."

This language has been repeated quarter after quarter and only the number changes. The company never gives a precise figure but always says "in excess of." For your information, the year-on-year growth in online sales given in each of the last nine quarters are shown below.

These sales are not insignificant. As Kenra Investors pointed out, if we use simultaneous equations with the info we have, we can estimate that online sales are currently over $1bn! Furthermore, BBBY's e-commerce growth is actually ahead of U.S. E-Commerce Retail sales that has only grown 14-16% according to the U.S. Census Bureau (see data here).

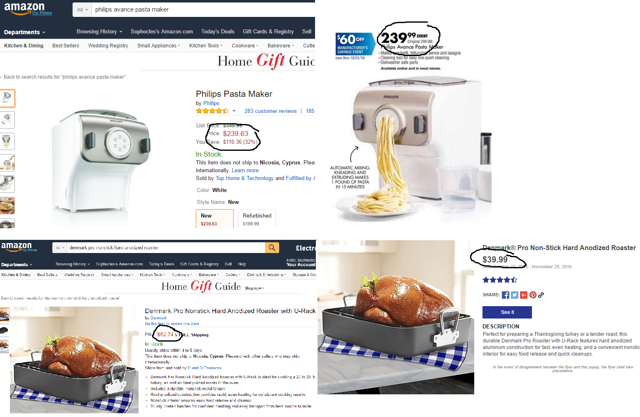

I decided to do some research on BBBY's online offerings. First, I browsed the online e-catalogs, which are currently the "October Circular," "Fall Book" and "Outdoor living." I started with the October Circular, and discovered the BBBY had decent prices. For examples, see below.

(Source: BBBY & AMZN websites)

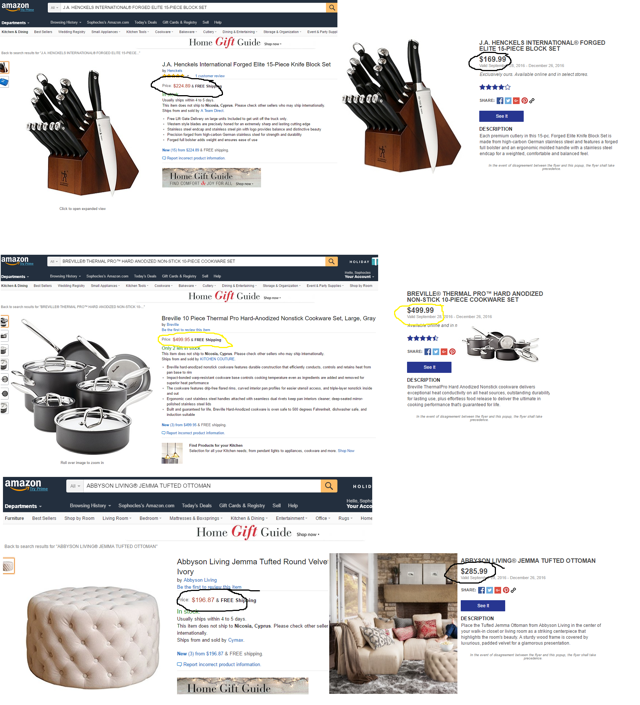

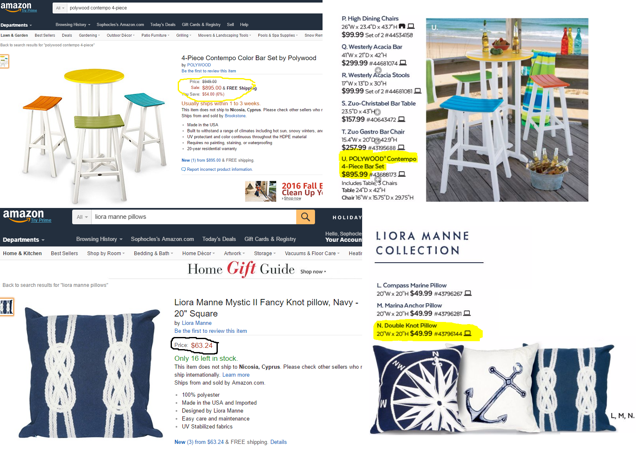

This got me curious and I started looking at items from the other 2 catalogs. Below are samples from the "Fall Book" and below that the "Outdoor Living" catalog.

(Source: BBBY & AMZN websites)

(Source: BBBY & AMZN websites)

(Source: BBBY & AMZN websites)

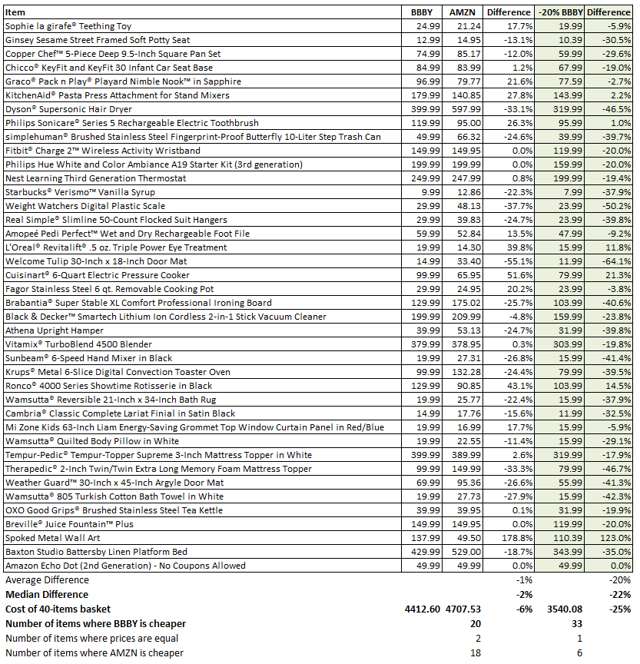

Could it be that Bed Bath & Beyond offered consumers better prices versus Amazon? If I were to discover the answer, I would need to look at a lot more products. As we know from statistics, we need at least 30 observations; therefore, I went ahead and collected 40. I picked random products from random categories on the BBBY website and then I would search for them on Amazon. For the entire basket, BBBY was 6.5% cheaper than AMZN!!!

On average, the list of items was 1% cheaper at BBBY (median cheapness was 2%). Shipping was not taken into consideration. All I did was look at the price of the items. If I had taken shipping into consideration, I suspect items would be even cheaper at BBBY because several items at amazon.com are sold by third parties with higher shipping rates.

BBBY has free shipping on orders over $29 and I don't think that is hard to achieve. Another issue (not documented but noticed) is the delay in shipping. For example, "Wamsutta® 805 Turkish Cotton Bath Towel in White" has a price of $22.55 (vs. BBBY $19.99) with an additional $5.78 shipping charge and "Usually ships within 4 to 5 days."

I do not live in the U.S. but it is my understanding that there are a lot of BBBY coupons circulating. If we take a 20% coupon into account then from our list of 40 products there are only 6 items, which are cheaper at amazon.com! Currently, BBBY is testing a paid subscription service (SA link, WSJ link). For $29 a year, a member gets 20% off all purchases and free shipping.

That would put my basket of goods at a 25% discount to Amazon (median item 22%) or a $1167 savings vs. AMZN! In the WSJ article, it states that Wedbush analysts believe BBBY would be on average 13% cheaper than AMZN (after the 20% discount). My research disagrees.

As my basket shows, the discount vs. AMZN already exists. I'll attach my excel with the basket to this article; however, it is my understanding only PRO subscribers are able to access attachments. If you are not a PRO subscriber, please contact me if you want a copy. Below is the list.

Management guidance for the year is $4.50 to just over $5.00 and this was kept the same in both the first two quarters. The Street estimates $4.74 and I agree based on the lower margins we have seen so far. BBBY with their recent marketing tests appear to be trying different things out. If they succeed and drive more people to their website and stores then margins will matter less.

The company has been buying back stock but I believe they should also pay a much higher dividend. The higher dividend would attract investors seeking income and help support the stock. Current valuation levels are attractive and FCF generation may attract an activist. Investors are faced with a challenging investing opportunity, but as a value investor, I believe it is worth the risk.

Supporting Documents

- BBBY_ITEMS.xlsx

Disclosure: I am/we are long BBBY.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Comments

Post a Comment